Cyprus Property & VAT: When Do You Pay 5%, and When Do You Pay 19%?

Updated following Official Gazette publication of 27 February 2026 | Amendments in force from 1 September 2026

If you are buying, selling, or developing property in Cyprus, one of the most important questions you will face is how much VAT applies — or whether VAT applies at all. The answer depends on two things: what kind of property it is, and whether it qualifies as “new” or “old” under the law.

Two Regulations published in the Official Gazette on 27 February 2026 amend the Cyprus VAT Law to formally define what it means for a property to be “new.” This guide explains the full picture — when the standard rate of 19% applies, when the reduced rate of 5% is available, and when VAT does not apply at all — with worked examples throughout.

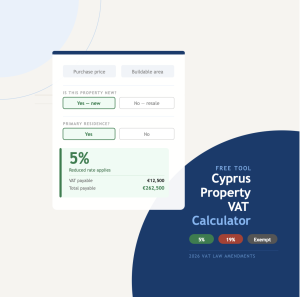

Cyprus Property VAT Calculator.

At a Glance: Which Rate Applies?

| Situation | VAT Rate |

|---|---|

| Buying a new property as your primary and permanent residence — within all caps (see below) | 5% on eligible portion |

| Buying a new property as your primary residence — but exceeding the overall size or value caps | 19% in full |

| Buying a new property for investment, rental, or as a holiday home | 19% |

| Buying an old / resale property (first occupied and used for at least 18 months) | Exempt |

| Renovating an old private home (at least 3 years since first occupation) | 5% |

| Renovating a property that is less than 3 years old | 19% |

Part 1: New vs Old — The Most Important Distinction

Whether VAT applies to a property sale depends first on whether the building is considered “new.” A new building — one that has never been properly occupied — is subject to VAT when sold. A used or old building is generally exempt from VAT on resale.

The 2026 amendments introduce clear statutory definitions for the first time:

First Occupation

The very first time a building is put to genuine, regular use after completion or handover. This includes the owner moving in, a tenant taking possession, a business operating from the premises, or any other systematic use of the property.

First Use

The building has been systematically occupied or exploited for a continuous period of at least 18 months. Only after this threshold is crossed does the property fully transition from “new” to “used” for VAT purposes.

In plain terms: a building does not become “old” the day someone moves in. It must have been continuously and genuinely occupied for at least 18 months before it loses its “new” status.

What this means in practice

❌ Example — treated as new, VAT applies

A developer completes a residential building in March 2025. One unit is rented to a tenant in April 2025, but the tenancy ends after only 10 months. The building has not yet reached the 18-month “first use” threshold. If the developer sells that unit in early 2026, it is still treated as a new property for VAT purposes.

✅ Example — treated as old, VAT-exempt on resale

Petros bought a new apartment in 2019, moved in, and lived there for five years. He sells in 2025. The property crossed the 18-month first use threshold long ago. The sale is VAT-exempt — the buyer pays no VAT on the purchase price.

Note: A VAT-exempt resale does not mean the transaction is entirely tax-free. Transfer fees, stamp duty, or capital gains tax may still apply depending on the circumstances.

Part 2: The Standard Rate — 19% VAT

The standard VAT rate of 19% applies to the purchase of any new property that does not qualify for the reduced rate. The most common situations are:

- Buying a new property as an investment, for rental income, or as a holiday home

- Buying a new property as a primary residence but exceeding the caps that govern the reduced-rate scheme (explained in Part 3 below)

- Any off-plan purchase where the buyer does not intend to use the property as their permanent home

❌ Example — 19% VAT

Andreas signs a purchase agreement for a new apartment in Limassol. The building is under construction. He intends to rent it out as a holiday letting. Because the property is new and he is not purchasing it as his primary home, 19% VAT is charged on the full purchase price.

On a €300,000 property: VAT = €57,000

VAT also applies to economic transfers — not just title deeds

One of the important clarifications introduced by the 2026 amendments is that VAT applies whenever the economic reality of a transaction amounts to a transfer of a new building — regardless of how the deal is structured on paper. VAT is therefore triggered not only when a title deed is formally transferred, but also when:

- A buyer takes possession of a new property under a sale agreement, even before the title transfers

- A lease agreement includes an option to purchase

- An agreement provides for the future transfer of ownership

❌ Example — 19% VAT on a lease-with-option arrangement

Maria enters a lease-with-option-to-purchase agreement on a newly completed villa. She moves in and pays monthly rent, with the contractual right to buy at a fixed price within three years. Because this arrangement effectively transfers economic control of a pre-occupation building, VAT at 19% applies from the outset — structuring it as a lease does not change the VAT treatment.

Part 3: The Reduced Rate — 5% VAT for a Primary Residence

Cyprus offers a reduced VAT rate of 5% for individuals acquiring or constructing a property that will be their primary and permanent place of residence. This is a significant concession — but it comes with strict conditions and caps that must all be satisfied together.

The four caps you must meet

Conditions for the 5% reduced rate — all four must be satisfied

| Reduced rate applies up to | The first 130 m² of buildable area |

| Reduced rate applies up to | €350,000 of the transaction value |

| Total buildable area must not exceed | 190 m² |

| Total transaction value must not exceed | €475,000 |

The 5% rate applies to the first 130 m² and up to €350,000 of the purchase price. But if the property as a whole exceeds 190 m² in buildable area or €475,000 in total value, the reduced rate is not available at all — 19% applies to the entire transaction.

Additional eligibility conditions also apply:

- The property must be your primary and permanent residence in Cyprus — not a holiday home, investment property, or rental.

- You must be an individual purchasing for personal residential use.

- The reduced rate has not previously been applied to the same property by another buyer.

- The property must be a new building — one that has not yet been first occupied.

Worked examples

✅ Example 1 — 5% applies in full

Eleni is buying a newly built apartment of 95 m² in Nicosia for €220,000 as her permanent home. The property has never been occupied. Total area (95 m²) is below the 190 m² overall cap, and total price (€220,000) is below the €475,000 overall cap. All conditions are satisfied.

5% VAT applies to the full purchase price: VAT = €11,000

At the standard rate this would have been: €41,800 — a saving of €30,800

🔶 Example 2 — 5% applies to part, 19% to the rest

Nikos is buying a new house of 160 m² for €420,000 as his primary residence. Total area (160 m²) is within the 190 m² overall cap, and total price (€420,000) is within the €475,000 cap — so the reduced rate is available. However, it applies only to the first 130 m² and up to €350,000.

5% on €350,000 = €17,500 | 19% on the remaining €70,000 = €13,300

Total VAT = €30,800

❌ Example 3 — 19% applies in full (area cap exceeded)

Stavros is buying a new villa of 210 m² for €600,000 as his primary and permanent home. The total buildable area of 210 m² exceeds the 190 m² overall cap. The reduced rate is not available at all — 19% applies to the entire transaction.

19% on €600,000 = VAT of €114,000

❌ Example 4 — 19% applies in full (value cap exceeded)

Anna is buying a new apartment of 140 m² for €510,000 as her primary home. The size (140 m²) is below the 190 m² cap — but the total transaction value of €510,000 exceeds the €475,000 overall value cap. The reduced rate is not available.

19% on €510,000 = VAT of €96,900

Part 4: The Reduced Rate — 5% VAT for Renovating an Old Home

The 5% reduced rate also applies to renovation and repair works carried out on a private dwelling — but only if the property qualifies as “old.” The 2026 amendments clarify the rule precisely:

When is a home “old” for renovation VAT purposes?

A dwelling qualifies for reduced-rate renovation VAT once at least three years have passed since its first occupation. The 18-month “first use” period runs concurrently with this three-year period — not consecutively. There is no additional waiting time beyond three years.

✅ Example — 5% VAT on renovation

Christos owns a house that was first occupied in March 2020. By March 2023 — exactly three years later — the property qualifies as “old” for renovation purposes. He commissions a full interior renovation in 2025. The contractor charges 5% VAT on the works.

On €80,000 of renovation: VAT = €4,000 (instead of €15,200 at 19%)

❌ Example — 19% VAT on renovation (too soon)

Sophia’s apartment was first occupied in January 2024. She wants to renovate in mid-2025 — only 18 months after occupation. The three-year threshold has not yet been reached, so renovation works are charged at 19%.

She should wait until January 2027 to benefit from the 5% rate.

Summary: The Timeline from New to Old

| Stage | VAT Status |

|---|---|

| Completion: Building finished, never occupied | New — VAT applies on any sale (19%, or 5% if primary residence within caps) |

| First occupation begins — owner, tenant, or any systematic user moves in | New — 18-month clock starts running |

| Month 18: 18 months of continuous occupation reached | Property becomes “used” — resale is VAT-exempt |

| Year 3: Three years from first occupation | Renovation works qualify for 5% reduced rate |

The 18-month and 3-year periods run at the same time from the date of first occupation — there is no gap between them. If a property was first occupied in January 2025, it becomes “used” for VAT purposes by July 2026, and qualifies for the renovation reduced rate from January 2028.

Cyprus Property VAT Calculator – Calculate your payable VAT!

Quick Checklist: Which Rate Do I Pay?

Work through these questions in order:

- Has the property ever been occupied? If no — VAT applies. Move to the next question to determine which rate.

- Has it been continuously occupied for at least 18 months? If yes — resale is generally VAT-exempt. If no — still treated as new, VAT applies.

- Am I buying a new property as my primary and permanent residence? If yes — check all four caps: total area must not exceed 190 m² and total value must not exceed €475,000. If within those limits, 5% applies to the first 130 m² and up to €350,000; 19% applies to any excess. If either overall cap is exceeded, 19% applies to the whole transaction.

- Am I renovating a private dwelling first occupied more than three years ago? If yes — renovation works attract 5% VAT.

- None of the above? The standard rate of 19% applies.

This article is for general informational purposes only and does not constitute legal or tax advice. VAT treatment depends on individual circumstances, the specific terms of each transaction, and applicable law at the time of completion. Always consult a qualified Cyprus tax advisor or legal professional before making decisions.